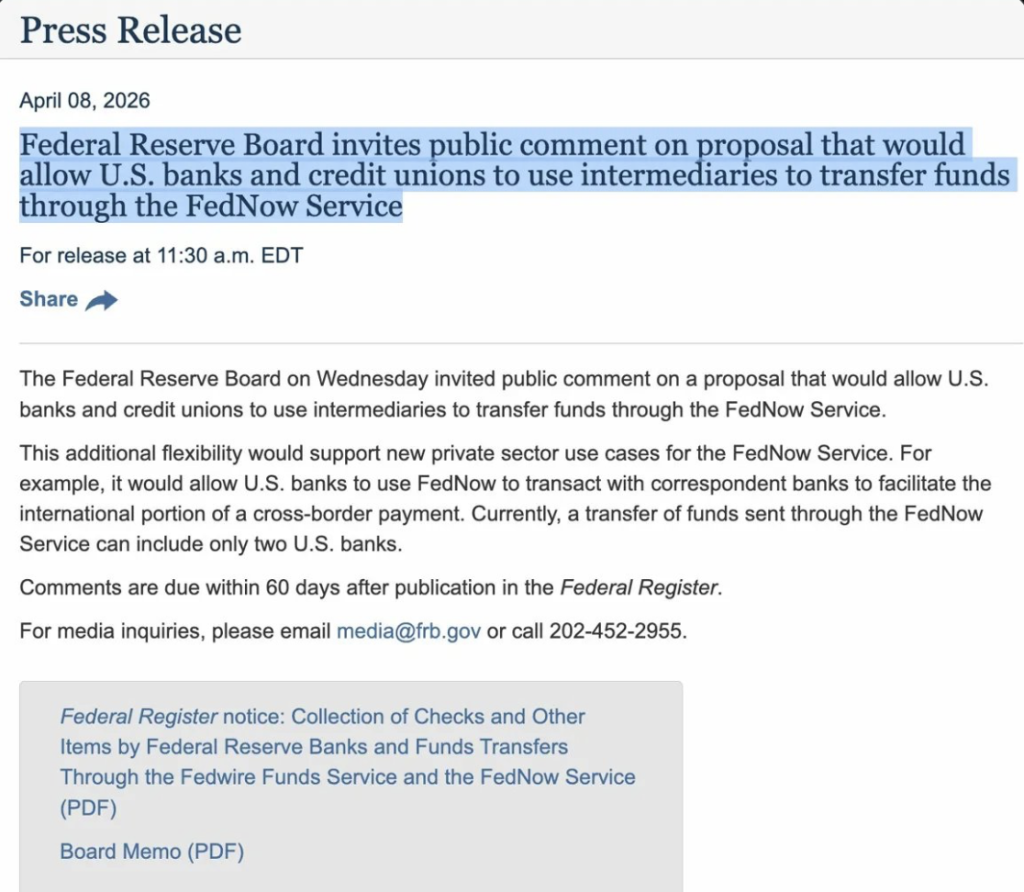

- The Federal Reserve is exploring FedNow expansion to include intermediaries and cross-border functionality

- Ripple’s conditional bank charter positions it to potentially integrate with Fed systems

- XRP’s role as a bridge currency aligns with evolving payment infrastructure trends

Something small just happened in the background of the U.S. financial system… and it might end up being bigger than it looks. The Federal Reserve is considering expanding FedNow, its instant payment system, and that change is starting to ripple—no pun intended—through the crypto space.

At first glance, it’s just a technical upgrade. But when you look closer, it introduces a new idea: intermediaries. Instead of limiting payments strictly between U.S. banks, the system could allow third parties to step in and help facilitate transfers, including potentially cross-border ones. And that’s where XRP starts to come into the conversation.

Ripple’s Setup Already Lines Up With the Shift

There’s an interesting alignment forming here. According to analyst XFinanceBull, Ripple is already positioned in a way that fits this evolving structure. Ripple National Trust Bank has been conditionally approved by the Office of the Comptroller of the Currency, which is a big step on its own.

If fully approved, that charter would allow Ripple to custody digital assets, offer lending, and—most importantly—connect directly to Federal Reserve systems like FedNow. That kind of access isn’t common, and it changes how Ripple could operate inside traditional finance.

The next piece, though, is still pending. Ripple needs a Fed Master Account, which would give it direct access to the Fed’s payment rails. Until that happens, it’s not fully plugged in… but it’s close.

A Bigger Picture Starts to Form

What makes this more than just speculation is the broader research backing it. A study published by the Financial Planning Association pointed out that Ripple and XRP could act as a bridge layer for cross-border payments, especially when tied into systems like FedNow.

Put simply, the Fed is exploring ways to expand payment infrastructure, and Ripple has already built technology that fits that exact need. It’s not about replacing banks or systems—it’s about connecting them more efficiently.

And that’s a subtle but important difference.

XRP’s Role as a Bridge Currency Gains Attention

Zooming out a bit, XRP’s use case keeps coming back to one core idea: speed and conversion. It’s designed to move value between different currencies quickly, whether that’s from something like the Iraqi Dinar or Vietnamese Dong into U.S. dollars.

That’s where it becomes useful—not as a replacement for fiat, but as a bridge between them. And as more financial systems look for faster, more transparent ways to settle transactions, that role becomes more relevant.

There are already signs of this in practice. Partnerships with companies like Temenos are starting to bring these systems into real-world banking environments, not just theory.

The Door Might Be Open—But It’s Not Fully Walked Through Yet

At this stage, everything feels… close, but not complete. The Fed is opening the door by expanding FedNow. Ripple has a conditional banking charter. The technology fits the direction things are moving.

But that final connection—the Fed Master Account—is still missing.

If that gets approved, things could shift quickly. If not, XRP remains on the edge of the system rather than fully inside it. Either way, the conversation is changing, and XRP is now part of it in a way that’s harder to ignore.