- Long-term Bitcoin holders remain inactive, signaling potential supply exhaustion in crypto markets.

- On-chain metrics show divergence, with weak price action but no major rise in coin movement.

- Whale profit-taking and steady retail sentiment point toward possible sideways consolidation rather than a crash.

At first glance, the crypto market looks surprisingly resilient. Despite ongoing global uncertainty, Bitcoin has been behaving almost like a safe-haven asset, holding steady while other markets wobble. That steady price action builds quiet confidence, the kind that doesn’t scream bullish but doesn’t look weak either.

But underneath that calm exterior, something more complex is unfolding. Data from Alphractal shows that while new retail traders and institutional capital remain active, coins that have been held for more than three years have nearly stopped moving. The Coin Days Destroyed metric, even on a 90-day average, has dropped to historic lows, signaling that long-term holders are neither reacting to volatility nor rushing to secure profits.

Supply Exhaustion or Just Investor Patience?

When you look deeper, this doesn’t feel like simple hesitation. It resembles supply exhaustion, where a significant portion of Bitcoin’s available supply is effectively locked away. Long-term holders are sitting tight, and that kind of stillness can shift market dynamics in subtle ways.

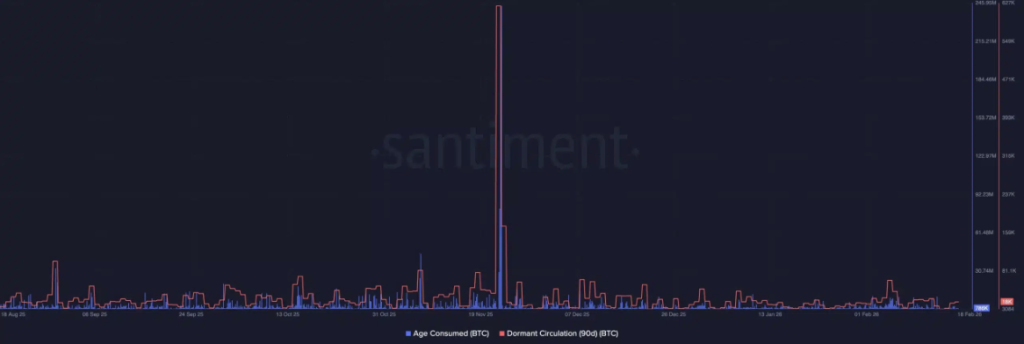

Other on-chain metrics add nuance. The Age Consumed metric showed older coins suddenly moving as Bitcoin pushed toward local highs in late November, breaking a long stretch of calm. At the same time, 90-day Dormant Circulation spiked sharply, suggesting some long-term holders used the rally as an exit point rather than a sign to double down.

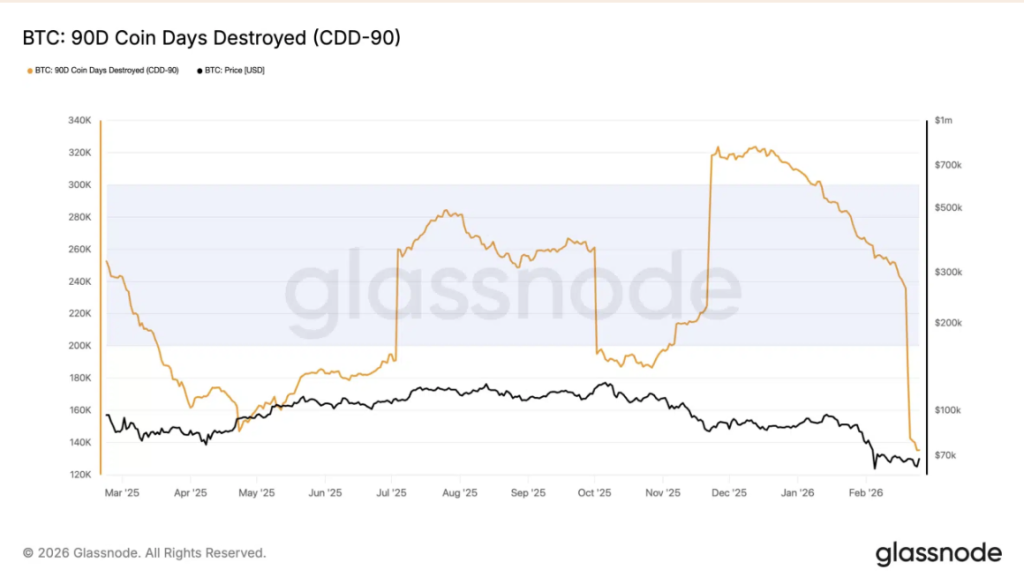

Glassnode’s data confirms that since December 2025, the 90-day Coin Days Destroyed (CDD-90) has fallen back to very low levels. What stands out is the divergence seen in February 2026. As Bitcoin’s price drifted toward the $70,000 region and weakened, CDD-90 did not rise. Normally, older holders react during stress. This time, they didn’t, which suggests most large-scale distribution may have already happened months earlier.

Mixed Crypto Sentiment Between Retail and Critics

Retail sentiment, interestingly, remains intact. Former JP Morgan employee Aditya Singhania recently noted that there is “absolutely zero panic in Bitcoin,” arguing that true fear would have shown up in crypto first if it were real. His view hints that the market may be positioned for a surprise, especially if expectations of a major drop fail to materialize.

Still, not everyone shares that optimism. Long-time Bitcoin critic Peter Schiff continues to question the asset’s resilience, reinforcing the divide between believers and skeptics. That tension between confidence and doubt feels like a defining theme of this cycle, and maybe that’s what makes it so hard to read.

Long-Term Holder Cost Basis and Whale Activity

Historically, Bitcoin often finds a true bottom near its Long-Term Holder cost basis, which currently sits around $38,900. With price still roughly 66 percent above that level, the market has not experienced the deep reset typical of previous bear cycles. Selling pressure appears to be coming mainly from short-term holders, while long-term investors remain steady, signaling pressure but not outright panic.

Meanwhile, whale behavior continues to shape the narrative. Lookonchain recently tracked an early investor selling 500 BTC worth about $47.77 million from a stash originally bought near $332. That is not fear-driven selling. It’s calculated profit-taking, gradually converting long-term gains into real-world wealth.

What’s Ahead for Bitcoin in 2026?

Bitcoin in 2026 feels like two markets operating at once. On one side are long-term holders who remain largely inactive and unmoved by volatility. On the other are early whales and short-term traders who are actively managing risk and locking in profits.

Unless global economic conditions worsen sharply, the most likely outcome is not a dramatic crash or explosive breakout. Instead, Bitcoin may enter a prolonged period of sideways movement, building pressure quietly before its next decisive move. It may not be exciting, but markets rarely move in straight lines for long.