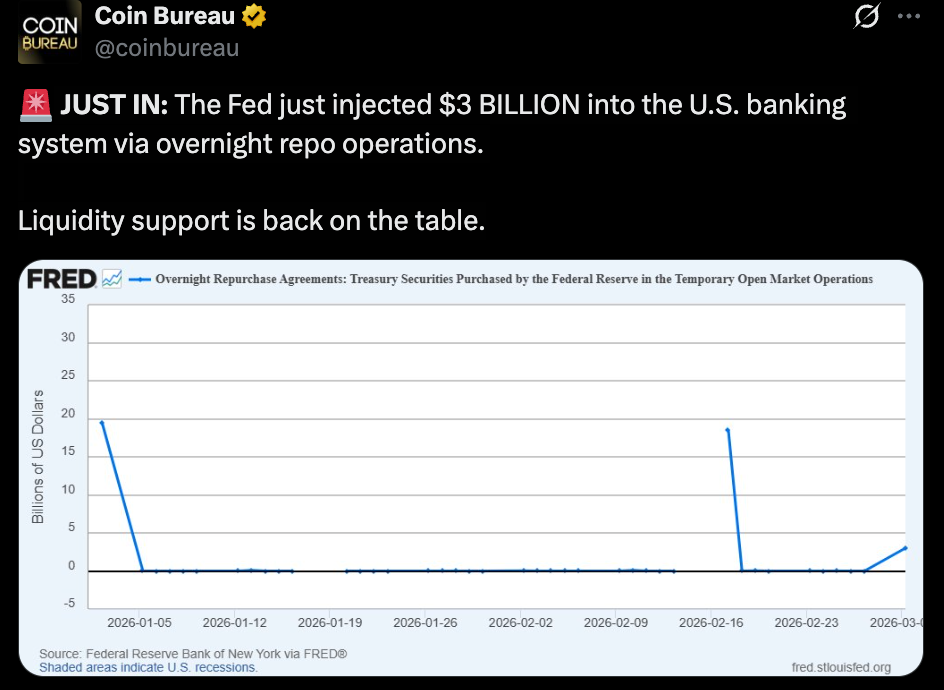

- The Fed added $3B through overnight repo operations

- Repo liquidity signals funding stress, not full QE

- Bitcoin’s muted reaction challenges the “money printer” narrative

The Federal Reserve injected $3 billion into the banking system through overnight repo operations. That move increases short-term liquidity by providing funding to primary dealers in exchange for high-quality collateral. It’s a stabilizing mechanism, not a dramatic policy shift.

This isn’t quantitative easing. It’s not a balance sheet expansion campaign. But it is liquidity entering the system, and historically, even small injections used to grab crypto traders’ attention fast.

The Old Bitcoin Playbook

For years, the thesis felt mechanical. When the Fed expanded its balance sheet, dollar liquidity increased. When liquidity increased, risk assets rallied. Bitcoin, often framed as a hedge against currency debasement, surged alongside expanding central bank balance sheets.

During 2020 and 2021, the relationship looked almost linear. Monetary stimulus rose, and Bitcoin went vertical. The narrative hardened into a rule: more money equals higher BTC.

Why Bitcoin Didn’t React

This time, the reaction was muted. A $3 billion repo injection barely moved Bitcoin’s price. There was no breakout candle, no sharp derivatives squeeze, no immediate surge in momentum.

The reason may be structural. Repo operations address short-term funding conditions, not long-term policy pivots. Bitcoin now trades more like a high-beta macro asset tied to ETF flows, derivatives positioning, and broader risk sentiment. Small liquidity plumbing adjustments no longer trigger reflex rallies.

A More Complex Macro Reality

Markets have matured, or at least evolved. The idea that every liquidity injection automatically lifts Bitcoin oversimplifies how capital actually moves. Institutional participation, regulatory clarity, and positioning dynamics now play larger roles than isolated funding operations.

If sustained liquidity expansion returns in a meaningful way, Bitcoin may respond. But a modest repo injection alone doesn’t guarantee upside. The old “money printer equals number go up” thesis was never fully automatic, it just looked that way during extraordinary stimulus cycles.